We can't find the internet

Attempting to reconnect

Something went wrong!

Hang in there while we get back on track

조 달러 방정식

요약

설명

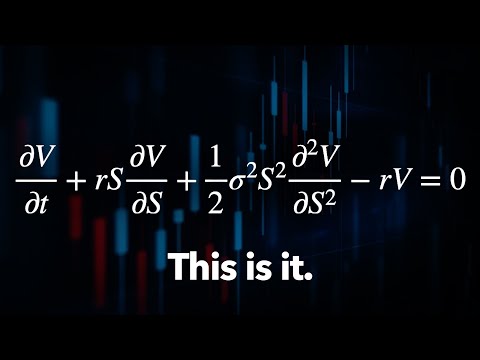

How the Black-Scholes/Merton equation made trillions of dollars. Go to https://www.eightsleep.com/veritasium and use the code Veritasium for $200 off your Pod Cover.

Special thanks to our Patreon supporters! Join this list to help us keep our videos free, forever:

If you’re looking for a molecular modeling kit, try Snatoms, a kit I invented where the atoms snap together magnetically - https://ve42.co/SnatomsV

▀▀▀

A huge thank you to Prof. Andrew Lo (MIT) for speaking with us and helping with the script.

We would also like to thank the following:

Prof. Amanda Turner (University of Leeds)

Owen Maher (Electrify Video Partners)

▀▀▀

References:

The Man Who Solved the Market: How Jim Simons launched the quant revolution, Gregory Zuckerman. Penguin Publishing Group. - https://ve42.co/GZuckerman

The Physics of Finance: Predicting the Unpredictable: Can Science Beat the Market? James Owen Weatherall. Short Books. - https://ve42.co/FinancePhysics

The Statistical Mechanics of Financial Markets, J.Voigt. Springer. - https://ve42.co/Springer

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of political economy, 81(3), 637-654. - https://ve42.co/BlackScholes

Cornell, B. (2020). Medallion fund: The ultimate counterexample?. The Journal of Portfolio Management, 46(4), 156-159. - https://ve42.co/Medallion

Images & Video:

Ed Thorp on The Tim Ferris Show - https://www.youtube.com/watch?v=CNvz91Jyzbg

Jim Simons on TED - https://www.youtube.com/watch?v=U5kIdtMJGc8

Jim Simons on Numberphile - https://www.youtube.com/watch?v=QNznD9hMEh0

▀▀▀

Special thanks to our Patreon supporters:

Adam Foreman, Anton Ragin, Balkrishna Heroor, Bill Linder, Blake Byers, Burt Humburg, Chris Harper, Dave Kircher, David Johnston, Diffbot, Evgeny Skvortsov, Garrett Mueller, Gnare, I.H., John H. Austin, Jr. ,john kiehl, Josh Hibschman, Juan Benet, KeyWestr, Lee Redden, Marinus Kuivenhoven, Max Paladino, Meekay, meg noah, Michael Krugman, Orlando Bassotto, Paul Peijzel, Richard Sundvall, Sam Lutfi, Stephen Wilcox, Tj Steyn, TTST, Ubiquity Ventures

▀▀▀

Directed by Will Wood and Derek Muller

Written by Will Wood, Emily Zhang, Petr Lebedev and Derek Muller

Camera operation by Raquel Nuno

Additional research by Gregor Čavlović

Edited by Jack Saxon and Trenton Oliver

Animated by Fabio Albertelli, Jakub Misiek, Ivy Tello, David Szakaly and Will Wood

Produced by Will Wood, Han Evans and Derek Muller

Thumbnail by Ren Hurley

Additional video/photos supplied by Getty Images and Pond5

Music from Epidemic Sound

번역된 시간: 2025-03-10T05:55:30Z

05:03

05:03